If you're selling a home, chances are you'll be on the hook for the realtor commission fee. The standard rate is approximately 6% of the home's final sale price. Of course, there are workarounds that can help you save big — you just have to know where to look.

The average real estate commission rate in the U.S. is about 6% of a home's final selling price, which is split down the middle between the listing and buyer's agents who handle the transaction.

Typically the seller is responsible for the full 6% fee — though in some situations there may be room for negotiation.

If you're looking to sell a home and save on commission, Clever can help!

We negotiate discount rates with top-rated agents across the country, saving you up to 50% on commission fees without sacrificing service.

> Learn more about low-commission real estate agents.

Read on for a more in-depth explanation of realtor fees: how much they are, who pays (and why), and all of your options for avoiding them.

Jump to a Section

- What are realtor fees?

- How much are realtor fees?

- Who pays realtor fees: the seller or the buyer?

- Are realtor fees negotiable?

- Are realtor fees tax deductible?

- 5 Ways to Save on Realtor Fees

- FAQs About Realtor Fees

What are realtor fees?

| Editor's Note: In this article, we refer to realtor fees and commissions interchangeably. This is because realtors charge no fees except for their commission, which is always a percentage of the final sales price. |

The majority of home sellers and buyers work with realtors who handle the sale on their behalf and represent their best interests. Though real estate agents are a warm and generous bunch, they can't provide this service for free. In return for their time, expertise, and attention, realtors ask for a cut of the profit made by the properties they sell: the realtor fee.

A realtor fee is also called a commission, because the fee is defined as a percentage of the property's sale price. In fact, this percentage is the only fee that realtors charge, so the term "realtor fees" is slightly misleading. Your realtor will never send you an itemized bill with obscure charges and hidden fees once the sale has closed.

It gets even simpler than that: because realtor fees are commission-based, neither sellers nor buyers owe any money to their realtors until a sale goes through. In other words, you'll never pay a cent to your realtor until they've earned it.

Clever negotiates discounted rates with top-rated, local agents across the country from major brands like Keller Williams, Coldwell Banker, and RE/MAX. You get full service and support — i.e., all the benefits and help you’d expect from a traditional agent — but for a fraction of the typical cost, saving you 50% (or more) on listing fees.

Full service includes pricing strategy, MLS listings, digital marketing, professional photography, showings and open houses, help with negotiations, paperwork, and more! Clever sellers save an average of $7,000 per transaction — and get offers 2.8x faster than the national average.

Want to learn more? Fill out the form below to get in touch.

How much are realtor fees?

There are no state or federal laws dictating commission rates, so in theory realtor fees can vary based on market, brokerage, agent, property, and any number of other factors.

In practice realtor fees are nearly uniform nationwide, and total 5-6% of the sales price. In the most common case, the seller's agent and buyer's agent will split a commission of 6%, with 3% going to one and the remaining 3% to the other.

Though the total commission and the way it's partitioned can change on a case-by-case basis, it will rarely vary by more than one or two percentage points from this industry standard of 6%.

> Learn how to save 50% on realtor commission fees WITHOUT sacrificing service.

What services do realtors provide in exchange for their fee?

Most realtors don't earn a salary or indeed any income other than their commission fees — which, of course, they only earn when they make a sale.

On the contrary, realtors often spend money in pursuit of a sale. Seller's agents devote a marketing budget to each property they sell, which comes out of their commissions (or out of their pockets if they're unable to close a deal).

This is to say nothing of the expertise realtors bring to the table, nor the time, sweat, and hustle it takes to sell a house. However significant realtor fees seem (6% of a property's price is certainly no chump change), the theory is that the value realtors provide exceeds the value lost to commission.

This theory is well tested: 87% of home buyers and 91% of home sellers opt to work with realtors. Buyers work with realtors to find the best property at the lowest cost, and sellers work with realtors to fetch a higher sales price, faster, for the least amount of hassle. For this group, the cost of paying realtor fees can be thought of as a further investment into their highest-value asset: their home.

> Learn more about the difference between seller's and buyer's agents.

Realtor Fees: A Brief History

The history of how commission evolved to today's model is quite interesting — dating back in the 1800s when local brokers began gathering at meeting halls to swap property information hoping to find a buyer offering the best price.

As these meetings expanded, in 1908 the predecessor of the current National Association of Realtors (NAR) created the multiple listing service (MLS) to share information about available listings. However, the MLS and all property information became exclusive to real estate agents instead of staying open to the public.

Because only licensed realtors could access the MLS, it laid down the groundwork for how agents could get paid — the listing agent would take a percentage of the sale and dictate the buyer's agent cut if their client bought the home. By controlling property information, realtors were able to set their own terms.

While today's commission model by and large maintains the same concept from the first commission design, technology has expanded what the traditional commission model can look like, giving sellers more flexible options when selling their home.

Who pays realtor fees: the seller or the buyer?

Just as realtor fees themselves can vary, so too can the specific commission structure of any given property deal. However, in almost every case, the seller is responsible for paying all realtor fees — even those owed to the buyer's realtor.

This means the property seller pays the full 6% realtor commission, which is subtracted from the final sales price and shared between the seller's agent and the buyer's agent.

Why is this the case? Because the buyer's agent is just as important to the home seller as their own realtor. No buyer's agent means no buyer, and no buyer means no sale.

Sellers offer a commission to buyers' agents in order to incentivize those agents to show off the property to their clients — i.e., potential buyers. While sellers aren't required to pay this commission, in practice they don't have much choice. If they insist that a buyer pay thousands in realtor fees in order to purchase their property, that buyer will more often than not say thanks but no thanks (that is, if their realtor even bothered to show them around).

Attracting buyers is fundamental to selling a home, and that means attracting buyers' agents with a lucrative commission. Knowing this, most sellers build the cost of realtor fees into the listing price for their home.

Do buyers ever pay realtor fees?

Buyers are typically never on the hook for realtor fees, which helps to explain why a decisive 87% of home buyers choose to work with a realtor. Because sellers build the full cost of realtor commissions into their listing price, buyers who choose to work without a realtor may wind up paying for representation they never even had.

Most buyers are aware of this fee structure, and some attempt to use it in their bargaining. For example, a buyer working without a realtor may submit a lower offer on the grounds that the total commission can be cut in half.

On the other hand, a buyer working with a realtor may really love a property and want to sweeten the pot: their bid may include an offer to cover their own realtor fees. That way the seller is only responsible for their own realtor's commission, and can keep an extra 3% profit on the sale.

| Editor's Note: As always, exceptions apply. If you use an agent to buy a property, the property seller is responsible for covering your agent's commission. However, if you're looking to rent a property and have employed a rental agent to aid you in your search, the story might be different. Sometimes landlords will cover your agent's fee, sometimes not. Sometimes it's up for negotiation, sometimes not. You'd be wise to discuss this with your rental agent upfront. |

Are realtor fees negotiable?

Realtor fees are negotiable by law — in that no state or federal laws limit or define them — but this doesn't mean that all realtors are willing to negotiate. Some listing agents will insist on a set price for their services and work only with sellers willing to pay it.

(Buyers, of course, don't need to negotiate because they don't pay realtor fees.)

Even realtors who are willing to discuss their fees may have their hands tied. Since realtors owe a percentage of their fee to the brokerage they work for (a commission on the commission, you might say), the brokerage may impose a minimum fee that prevents realtors from negotiating.

Where realtors are willing and able to negotiate, it's important to remember that negotiation is a two-way street; you'll likely have to offer something in return for paying a lower commission. Consider: if you find a realtor willing to cave to your demands to pay a lower fee, just because you demand it, do you really want to hire that person to sit in your place at the negotiating table?

When will a realtor lower their commission rate?

Each property sale is unique. Circumstances like market temperature, property value, and even the relationship between seller, buyer, and agent can determine whether or not a realtor is willing to accept lower fees. Under the right conditions, you may be able to haggle half a percentage point or more off of your realtor's commission. For example:

- Your property is particularly valuable, and your agent can make a killing even at a lower rate.

- Your property is in a white-hot market, and you believe it will basically sell itself.

- Your realtor represents you as both a seller and a buyer, so you're twice as valuable as a client.

- Your realtor represents both you as a seller and your buyer, so they're half as valuable as a realtor. (This is called a dual agency sale, and you should steer clear.)

- Your realtor just really, really likes you. (Maybe you're a close friend or simply buy and sell a lot of property — in which case this guide is likely of limited use.)

If none of the above is true for you but you're still looking for lower realtor fees, you can always ask your agent to provide a subset of their services in exchange for a reduced commission.

This might mean you have to give up professional advertising or staging, or that you decide to hold open houses yourself, or that your listing agreement is cut short.

At the extreme end of this — if you're particularly strapped for cash — you can hire flat-fee real estate agents who act in a purely transactional role for a much smaller fee. These agents will list your property on the MLS but do little else; the most expensive of them will also help you price your home and write out the sales contract.

While you can find lower realtor fees if you're willing to settle for fewer services, beware: the loss of these services can hinder your ability to effectively sell your property. You'll want to carefully consider whether you're giving up more value than you're saving.

How to Calculate Realtor Fees

Calculating realtor fees is as simple as multiplying the sales price of the property by the total commission rate to be split by both realtors (typically 6%). Who pays which part of these fees depends on the situation, but it's usually the seller.

Whatever the case, the math is as easy. If you sell your house for $250,000 at a standard realtor commission of 6%, you can simply plug those numbers into the following formula:

Realtor Fees = Sales Price x Total Commission

to get:

Realtor Fees = $250,000 x 6%

or equivalently

Realtor Fees = $250,000 x 0.06

which works out to $15,000. In the end, both your realtor and your buyer's realtor will wind up with $7,500 each — half of those total fees.

If you're selling your house, remember to account for these realtor fees when figuring out an appropriate listing price. Even if you're selling without an agent of your own, you're responsible for paying the buyer's agent's commission of 3%.

Are realtor Fees Tax Deductible?

In a word, yes.

From the IRS's Publication 523: Selling Your Home:

| "If you meet certain conditions, you may exclude the first $250,000 of gain from the sale of your home from your income and avoid paying taxes on it. The exclusion is increased to $500,000 for a married couple filing jointly." |

In other words, if you meet the right requirements, you can deduct the costs of selling your house from the taxable gains you earned in the sale. Eligible selling costs include, among other things, realtor fees.

Publication 523 has the full list of these requirements, and will help you determine whether you qualify for maximum or partial exclusion of gains. In short:

- The home you sell must have been your primary residence.

- You must have owned and lived in the home for two of the five years preceding the sale (meaning 24 months, not necessarily consecutive).

- You haven't taken a gains exclusion on the sale of a different property in the previous two years (the "look-back" requirement).

Naturally, there are plenty of exceptions, clarifications, and additional requirements to these rules. You should always consult with an accountant to determine which tax exclusions you personally qualify for.

> Learn more about the tax deductions you can take when selling your house.

5 Ways to Save on realtor Fees

1. Shop Around

Before you begin to worry about saving on realtor fees, you should figure out which realtors are worth paying fees to at all.

Survey the field by searching for realtors online, reading reviews of different brokerages and agents, and asking for recommendations from friends and neighbors. Once you've got a shortlist of potential realtors to work with, you can contact them directly to suss out who might be a good fit for your property. Ask them questions like:

- "How long have you been working as a realtor?"

- "How much experience do you have selling homes in my market?"

- "How many days does it take your listings to sell, on average?"

- "What would your pricing strategy be for my home?"

And the two most important questions if you're looking to save on realtor fees:

- "What is your commission rate?" and

- "Are you willing to negotiate?"

Be clear about your needs and goals as you shop around for the right realtor. Not only will this help you find an agent capable of meeting them, but you'll demonstrate a savviness that will serve you well in any eventual fee negotiations.

2. Negotiate Rates

Once you've found a realtor you feel good about working with — and who's willing to discuss their fee — you can begin to negotiate.

To do this effectively, you'll need to understand the state of your local housing market, the value of your property, and the added value your realtor will bring to the sale. Ideally, that means doing your homework and studying the listing price, time on market, advertising strategies, and ultimate sales price of comparable homes in your area. You can't expect to negotiate unless you have an idea of what you're getting yourself into.

From there, you'll have to decide what you want from your realtor and what you're willing to offer in return. Which leads us to:

3. Consider Your Needs

You may not need all the services a realtor provides, and if you don't, why pay for them?

If all you want is for a licensed real estate agent to list your property on the MLS, then you can get away with paying a flat fee instead of a full commission (though note that working without a realtor may cost you in other ways).

On the less extreme side of things, a realtor may be willing to lower their commission if you're willing to lower your demands. You can make yourself a less intensive client by forgoing certain non-critical services, like open houses or professional advertising. If they're amenable, less work for your realtor can mean lower fees for you — but just remember you'll have to pick up some of the extra slack yourself.

> Get more tips for negotiating fees with your realtor.

4. List for Sale by Owner (FSBO)

The most straightforward way to save on realtor fees? Don't hire a realtor.

The simplicity of this approach makes it a common tactic. Over a third of all home sellers in the United States attempt to list their properties this way, referred to as For Sale By Owner (FSBO). These intrepid sellers take on all the hard work of a listing agent — pricing, staging, showing, negotiating, etc. — in return for the added profit they hope to earn by not paying a realtor's commission.

Appealing as this scheme sounds, in reality just 11% of sellers who list FSBO — less than a third of those who try — find success. The rest, after weeks or months of hard work and dissatisfying results, cut their losses and turn to a realtor with experience in their market.

And don't forget that even sellers who close the deal themselves must still pay the buyer's agent's 3% commission, as well as their own share of closing costs. And whether or not their final profit is greater than it would have been with a realtor — even when accounting for the extra commission — is difficult to say.

CONSIDER THIS: In 2017, the median sales price for homes listed with a realtor was $265,000. For homes listed FSBO, the median sales price was just $200,000 — a full $65,000 less.

Still keen to give FSBO a try?

> Read our in-depth guide on how to sell a house without a realtor.

5. Work with a Trusted Agent Referral Network

A real estate referral network connects a brokerage with a high volume of clients in return for a cut of the commission those clients bring in. And because the brokerage doesn't have to spend time or money acquiring those clients, they can offer their services at lower fees while still turning a profit.

Semya-Moya is a leading real estate referral network that works with major brokerages all across the country. Clever Partner Agents are top-rated realtors who provide their full range of services at significantly lower fees than traditional agents — no haggling, negotiating, or compromising required.

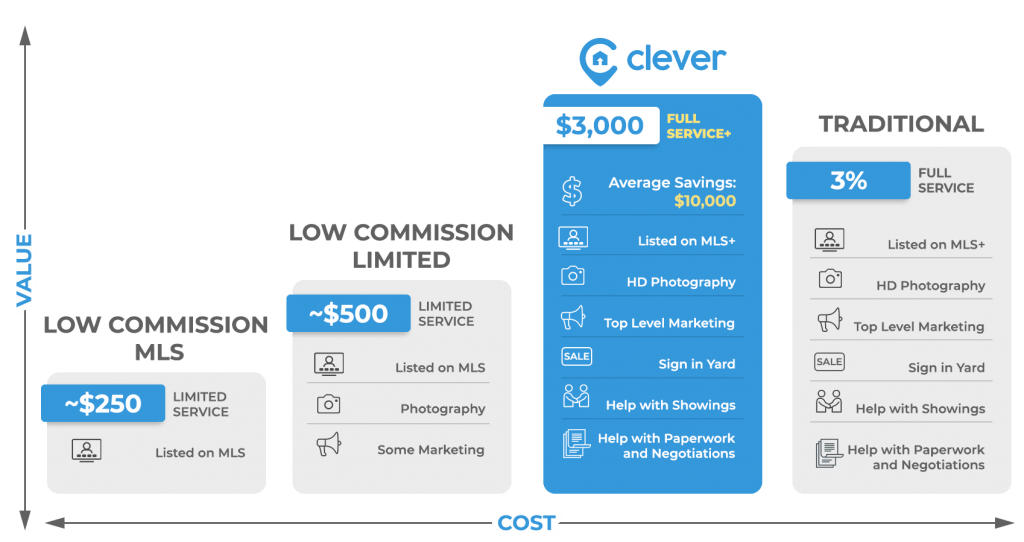

See how Clever Partner Agents stack up against other low commission realtors:

For sellers looking to lower their realtor fees, Clever Partner Agents provide the full value of a listing agent for a flat fee of $3,500, or just 1.5% commission on sales greater than $350,000.

Clever sellers save an average of $7,000 per transaction — and still manage to get offers 2.8x faster than the national average.

> Get in touch to learn more and connect with agents.

How are realtor fees different than closing costs?

Realtor fees are the percentage of the sales price paid to realtors in a property transaction. While this commission is only paid out once the sale has closed, it doesn't count as a closing cost because it isn't incurred as part of the closing process — it's simply the realtor's agreed-upon fee.

Contrast this with actual closing costs, which are miscellaneous fees that differ from property sale to property sale and arise in the regular course of doing business. Closing costs include fees associated with surveying, title searches, deed recording, loan processing, insurance, and more — even prorated property taxes and homeowners association fees can count.

Because these closing costs can vary greatly between sales, they'll range anywhere from (generally) 2-7% of the sales price. And unlike realtor fees, which are standardly paid by sellers, the distribution of closing costs is much more open to negotiation. In fact, keeping your share of closing costs as low as possible is part of how your realtor will earn their fee in the first place.

> Learn more about who pays closing costs.

How much are closing costs for the seller?

Closing costs for sellers are typically lower than those for buyers: approximately 1-2% of the sales price of the home. But keep in mind that these closing costs are on top of any realtor fees, so sellers are still getting the short end of the stick here.

Some common closing costs typically paid by the sellers include:

| Fee | Description | Typical Cost |

| Title Search | This confirms the seller is the legal owner of the property and makes sure there are no outstanding liens on the home that would prevent a clean sale. | $300-$500 |

| Title Insurance | A one-time fee, title insurance protects the buyer from any issues with your home's title such as liens or property ownership disputes. | $750-$2,000 |

| Home Inspection | Home inspections verify the condition of the house and check for any necessary repairs. | $300-$500 |

| Home Appraisal | A report by a licensed appraiser verifies the property's value. Note that this is usually required by lenders, and since the fee is paid directly to the appraiser, it will be nonrefundable even if the loan is not secured. | $450-$650 |

| Survey | In some states, lenders require a survey, which maps the property lines and legal boundaries. Some states also allow a survey affidavit to be substituted. In a survey affidavit, the sellers essentially swear that the property's boundaries have not been changed during their ownership. Costs may vary, but expect to pay about $50. | $250-$500 |

| Credit Report | This fee goes to the lender for running a credit report check to verify the buyer's credit. | $25-$50 |

| Loan Payoff Costs | These are charged by the lender to cover processing the buyer's loan. They include an origination fee to cover the lender's costs during the underwriting process, as well as smaller fees for the loan application and for prepaying the first month's interest. | Varies, Around 0.5-1.5% of the Home Price |

| Mortgage Payoff and Prepayment Penalty | Sellers will pay any amount remaining on their home mortgage at closing. Note that some lenders charge a penalty for prepaying your loan before the end of its term. You should check with your lender to see if there are any such penalties, and what the cost will be. | Varies |

| Outstanding Amounts Owed on the Property | These include bills such as property taxes, utilities, homeowners insurance, and HOA dues (if applicable). These will be prorated so the seller is responsible until the date of closing. | Varies |

| Transfer Taxes | This is the tax for transferring the title from you to the buyer. While not every city or state charges transfer tax, the nation's average is $750. Learn more about transfer taxes here. | Varies |

| Recording Fees | These cover your title company, escrow agent, or attorney filing the deed of property transfer with the county. This is usually a modest fee, set by each county. | Varies |

| Settlement or Attorney Fee | The settlement fee is paid to the title company or escrow agent for their services handling your closing. This typically amounts to about 0.2% of the sale price. Some states will also require an attorney for closing. Attorney fees vary, but typically range between $150-500 for this type of service. | Varies |

How much are closing costs for the buyer?

In general, buyers will usually pay the majority of a sale's closing costs — somewhere in the area of 3-4% of the sales price. This list of closing costs for buyers includes:

- Lender's title insurance policy

- Recording fees

- Surveying costs

- Inspection costs

- Homeowners insurance

- Homeowners association fees

- Lender fees

When you apply for a mortgage, your lender will provide you with an estimate of your total closing costs — what used to be known as a "good faith" estimate (nowadays it has the less snappy title "Loan Estimate and Closing Disclosure Form"). If you need, you have the option of rolling these closing cost obligations into your mortgage.

How to Calculate Closing Costs

Because closing costs differ so drastically between sales, it can be difficult to calculate them accurately. This is made even trickier by the fact that who pays these costs can also vary from deal to deal.

As a simple example, let's assume that a house sells for $300,000 and that the seller's and buyer's shares of closing costs are a typical 2% and 4%, respectively.

In this case, the seller pays $300,000 x 2% in miscellaneous closing costs, which equals $6,000.

The buyer pays twice as twice: $300,000 x 4%, or $12,000.

Total closing costs on this sale are thus $6,000 + $12,000 = $18,000.

Check out how closing costs can scale with sales price:

| Sales Price | 1% Closing Costs | 2% Closing Costs (Typical Seller's Share) | 3% Closing Costs | 4% Closing Costs (Typical Buyer's Share) |

| $150,000 | $1,500 | $3,000 | $4,500 | $6,000 |

| $250,000 | $2,500 | $5,000 | $7,500 | $10,000 |

| $350,000 | $3,500 | $7,000 | $10,500 | $14,000 |

| $450,000 | $4,500 | $9,000 | $13,500 | $18,000 |

Remember that whether you're selling or buying, your realtor is working to negotiate where you fall on this spectrum of closing costs. As you can see, this can mean a difference of thousands of dollars in additional fees.

Are closing costs tax deductible?

Certain closing costs can be subtracted from the gains you earn when you sell your house. Because these qualify as selling costs, they offset your profit on the sale and reduce your tax burden — that is, if you meet the eligibility requirements.

(Refer to the section "Are realtor fees tax deductible?" for more information on these eligibility requirements.)

But be careful: not all closing costs can be deducted from your capital gains. The IRS is happy to grant you the following cost deductions:

- Utility service installation charges

- Title search fees

- Costs for preparing the sales contract and deed

- Survey fees

- Owner's title insurance

Whereas these are costs you'll simply have to swallow:

- Moving expenses

- Mortgage fees

- Fire insurance premiums

- Utility service charges before closing the sale

All applicable deductions are detailed in Publication 523: Selling Your Home, which is available for download on the IRS website. You would be wise to review it and speak to an accountant for more personalized information.

Save Thousands on Realtor Fees with a Low-Commission Agent

Working with a quality realtor — whether you're selling or buying a house — means less time on the market, fewer gray hairs on your head, and more money in your pocket. If you want that payoff but aren't so keen on paying for it, Clever can help.

Clever is a leading real estate referral company that works with top-rated realtors across America. Through Clever, home buyers and sellers alike can find full-service real estate agents from major brokerages like RE/MAX, Keller Williams, and Century 21. These Clever Partner Agents — who ordinarily take a full commission of 3% — have agreed to charge far less to clients who connect with them through Clever.

How much less? If you're selling your home, Clever Partner Agents work for a flat fee commission of just $3,500 — or 1.5% if the total sales price exceeds $350,000. At that price point, Clever would save you a full $6,750 in realtor fees compared to working with a traditional agent for a traditional commission. And as the sales price goes up, so do your savings:

| Sales Price | Traditional Seller's realtor Fee (3%) | Clever Partner Agent realtor Fee ($3,500 or 1.5%) | Clever Saves You |

| $150,000 | $4,500 | $3,500 | $1,000 |

| $250,000 | $7,500 | $3,500 | $4,000 |

| $350,000 | $10,500 | $3,500 | $7,000 |

| $450,000 | $13,500 | $6,750 | $6,750 |

Top FAQs About Realtor Fees

Do buyers ever pay realtor fees?

In a typical property sale, buyers are not responsible for covering their realtor's fees. Instead, both realtors split the total commission paid by the seller — generally 6% — which is subtracted from the sales price once the deal has closed.

However, there are a few scenarios in which buyers may end up paying their own realtor's fee:

- The seller is not willing to pay the full commission. Some sellers will insist, as a condition of purchasing their property, that buyers pay their own agent's commission. Many buyers (and buyer's agents) simply skip these properties.

- The buyer offers to pay their own realtor. On the flip side of this scenario, a purchase offer that includes an extra 3% of the sales price (the buyer's agent's share of commission) is very enticing to sellers, and makes a bid stand out.

- Both parties arrive at a separate agreement. At the negotiating table, everything is up for discussion: sales price, closing costs, contingencies — and who pays the realtors. Though atypical, an agreement to share commission costs between seller and buyer (for whatever reason, and however split) is always a possibility.

Are realtor fees included in closing costs?

realtor fees are not included in closing costs, which instead comprise all the other miscellaneous costs buyers and sellers incur in the course of closing a property sale — costs like title insurance policies, prorated utility charges, escrow fees, and more.

The specifics of these fees — and who's responsible for paying them — differ greatly between deals. Typically, closing costs will range between 2-7% of the final sales price, split in some way between the seller and the buyer.

How are realtor fees calculated?

Because realtor fees are commission-based, you only need two pieces of information to calculate them: sales price and commission rate. The formula is dead simple:

Realtor Fees = Sales Price x Total Commission

Total commission is typically 6% shared between the seller's realtor and the buyer's realtor. In most cases the seller pays this full fee, deducted from the sales price.

A quick example: If you sell your home for $200,000 at the standard commission rate, your total realtor fees would be $200,000 multiplied by 0.06, which equals $12,000. Note that this doesn't include any of the other costs associated with selling your house, like repairs and closing costs.

What expenses can you write off when you sell your home?

If you're selling your primary residence (and not, say, a rental property), you can write off many of the costs associated with maintaining, improving, and selling the home.

These deductible selling expenses include certain closing costs (like title insurance, inspection expenses, and legal fees) and — even more important — realtor fees. Some selling costs, on the other hand, aren't deductible; moving expenses are a good example.

Since the type and extent of selling costs are different for every property sale, you should always consult with your realtor and accountant to figure out which expenses you'll be able to write off.

> See what is (and isn't) tax deductible when you sell a house.

How much do I pay a realtor to sell my house?

As the seller, you're typically responsible for paying not only your own realtor but your buyer's realtor as well.

What you owe each of these realtors depends on the sales price of your house, which means you don't pay a dime until your house actually sells. When it does, each realtor is entitled to a percentage of the final sales price — generally 3% each. Both those realtor fees add up to a total of 6% of your house's sales price.

In other words: For every $100,000 your home sells for, you'll pay $6,000 in fees using a traditional realtor.

Can you negotiate realtor fees?

Yes, you can negotiate realtor fees — if you can find a realtor willing to negotiate. Some realtors simply aren't interested, and this will depend on their level of experience, their track record in your market, the value of your property, and other factors.

If your realtor is willing to negotiate their standard 3% commission, you'll likely have to settle for fewer services in return. For example, your realtor might agree to work for 2.5% commission in exchange for a reduced advertising budget or an agreement that you hold open houses on your own.

If all you need is a single service — namely, having your property listed on the MLS — you can even get away with paying a flat fee instead of a commission. But this is less a negotiation with a realtor than a tactic for trying to sell your home without one.

There's a better option. If you work with a Clever Partner Agent, you don't have to negotiate realtor fees or compromise on services. With Clever, you pay a flat fee of just $3,500 for a full-service realtor, or 1.5% if your home sells for more than $350,000.

> See more tips for negotiating fees with your realtor.

How do you avoid realtor fees?

If you're in the market for buying a home, good news: you don't have to worry about realtor fees at all. Sellers are responsible for paying both realtors in a property transaction.

On the flip side: If you're selling, unfortunately, you're on the hook for two fees. But that doesn't mean you don't have options to avoid them, or at least cut them down. Here are a few ways you can go about it:

- List your property For Sale By Owner. You won't have to pay your realtor if you don't have one, but selling your house will be a lot more work. And don't forget, you'll still have to pay your buyer's realtor. Unless of course you…

- Make the buyer pay their own realtor's fee. This will shave 3% off of your total realtor costs, but from a buyer's perspective, that 3% is simply added onto the price of your property. Don't be surprised if this rubs prospective buyers the wrong way and makes your house a harder sell.

- Work with a full-service, low-commission realtor. If you want a realtor's help selling your home and you don't want to dissuade buyers at the door, your best bet for avoiding fees is to find a realtor willing to work for less. Enter Clever: a leading real estate referral company that partners with top-rated realtors from major brokerages all across the United States. Clever Partner Agents provide their full suite of home selling services at a fraction of the cost of traditional realtors: just $3,500 or 1.5% if the sale is greater than $350,000.

What part of closing costs are tax deductible?

While many closing costs on the sale of your house are tax deductible, not all of them are. This can be confusing when it comes time to claim.

Some of the major closing costs you can deduct include:

- Title insurance

- Title search fees

- Survey fees

- Sales contract costs

The following costs, however, are not tax deductible:

- Moving expenses

- Mortgage fees

- Credit report costs

For a more complete picture of which closing costs are tax deductible and which aren't, read through the IRS's Publication 523: Selling Your Home (or better yet, talk to your accountant).

Are realtor fees tax deductible for rental property?

To recognize the importance of home ownership, the IRS allows realtor fees to be tax deductible when selling your home — but only under certain circumstances.

One of the main eligibility requirements says that the home you sell must be your primary residence, and unfortunately that takes rental properties off the table. However, you may be eligible for tax deductions if you only rent out a portion of a property that otherwise qualifies as your primary residence.

While you might not be able to write off realtor fees for a full rental property, real estate investors have come up with plenty of other strategies you can use to minimize your tax burden. For example, you can buy and sell properties with a family member in a lower tax bracket, offset your rental income with other financial losses, or engage in something called a 1031 exchange.

> Learn more about tax deductions on investment properties.

Do you pay realtor fees out of pocket?

If you're buying a house, you can work with a realtor at no personal cost. This is because your realtor works on commission, and gets paid by the seller of any property you buy.

If you're selling a house, on the other hand, you're responsible for paying fees to your realtor and your buyer's realtor both. This total commission is generally 6% of the sales price, but you don't pay it out of pocket. Since you don't owe either realtor any money until your house sells, the fees are simply subtracted from the sales price once the deal has closed.

To compensate for this lost profit, sellers usually build the cost of realtor fees into the listing price for their property.